A long-awaited inflection point for the downtown Seattle housing market occurred in 2021 following three years of political dysfunction, an economic downturn, and value corrections. These headwinds were propelled by adverse tax policies and civic budget cuts, social unrest, and of course, the COVID-19 pandemic, which all combined in 2020 and resulted in a net loss of 8,000 residents from downtown Seattle. That’s all reversing course now.

The promise of a new mayor (and several City Council seats), renewed investment in social services, and the reopening of businesses and lifestyle attractions, brings with it improved consumer confidence and increased housing demand to the city center. It helps too that developer discounts and incentives at both newly delivered apartment and condominium buildings have been coupled with historically low interest rates and a booming stock market. Savvy, in-bound residents pounced on attractive housing opportunities with increased purchasing power. Discounts on new condominiums with deferred HOA dues and free rent periods on apartments are becoming harder to find. Such opportunities remain for now, but perhaps not for long.

Downtown Seattle is experiencing an extraordinary comeback as the region’s urban employment center draws thousands of workers back (55% of Seattle’s jobs are downtown while it occupies just 6% of the landmass). Shockingly, the metro area experienced two years of traditional apartment demand during the first half of 2021, according to O’Connor Consulting Group, and downtown Seattle’s apartment vacancies dropped from more than 8% at the end of 2020 to just over 3% today. Rents have returned to pre-pandemic values, averaging $3.80 per square foot per month, with lease rates expected to increase 15% by 2023. Despite thousands of new apartment units nearing completion, Brian O’Connor, Principal of O’Connor Consulting Group, believes the market is “at equilibrium” and he only expects a slight uptick in vacancy rates by 2023. O’Connor says new rental demand will remain high as will job growth, but some renters will want to take part in rising condominium prices, so a migration from rent to own is also likely ahead. It may already be happening.

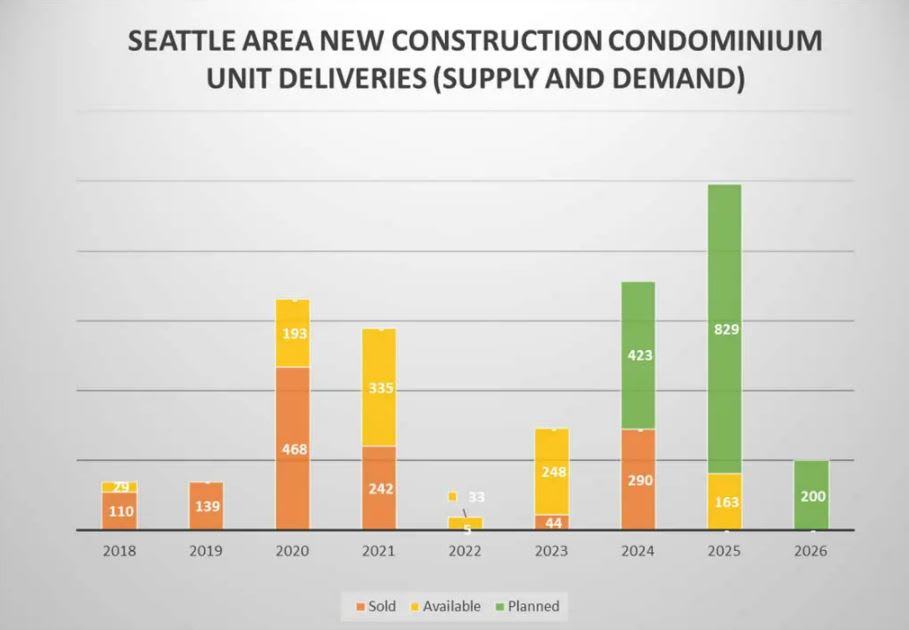

The cohort of new, move-in-ready condominiums experienced a 415% increase in pending sales in 2021 compared with the same period in 2020. Currently, 59% of the 2,218 new units across 11 active developments have already found a buyer, and two active and recently completed condominium projects were converted to apartments to take advantage of the upswell of rental demand. Furthermore, at least two more condominium towers that were being tracked in the pipeline, also reverted to rental. At this point, it now appears fewer than 1,500 new condominiums are likely to be added to the market by 2026, and that’s if they all get built. Total unit deliveries have been in steady decline since 2019.

The resales of existing condominiums also show dramatic improvement with active inventory declining 61% year-to-date in 2021 over 2020, while pending sales have soared 46% during the same period. Prices, while about 4% lower than a year ago, have stabilized and will likely trend higher again as bargain hunters were the first to seize the preferred selection at corrected values (the bottom of the market has already passed, as it has in other major metro areas like San Francisco and Manhattan). Power broker Nikki Field of Sotheby’s International Realty said, “New York is beyond back.”

Now the challenge with high-rises is the demand can rise much quicker than supply (it can take five years to assemble land, secure entitlements and construct a tower for occupancy). As the current housing cycle ends with final unit deliveries in 2022, and only a few buildings are underway for the next development boom, it will likely take several years to manifest a meaningful supply of either new apartment or condominium towers. O’Connor asserts construction hard costs have risen by more than 30% over the past two years, in part due to COVID-era protocols, but also because of inflation of raw material prices, labor shortages and union strikes, and protracted development schedules. Construction lending is also tightening. The bottom line is that both rents and condominium values will have to rise significantly to pencil new projects in the new market cycle. O’Connor believes a new condominium tower will need to average $1,500 per square foot during presales before any project in the condominium pipeline is likely to move forward. Again, just two new condominium towers are under construction with occupancy scheduled for 2023 and 2024, respectively. Approximately 45% of the 745 units being developed are already under contract with buyers.

Given rising construction costs, a similar development downturn can be found with rental housing supply. New apartment starts in Seattle have decreased 87% during 2021 compared with 2020, which is concerning considering this submarket historically captures 63% of the apartment demand for the Seattle-Bellevue-Everett area. More supply is needed to keep lease rates from swelling. To put this in perspective, 27,000 multi-family housing units were added to downtown Seattle during the last decade, of which approximately 93% was purpose-built for rent and not for sale. During this time, rents grew 50%, and while 2020 proved to be a speedbump in this upward trajectory, experts agree the marketplace has rebooted and rents are on the rise again.

The Downtown Seattle Association predicts more than 100,000 residents will be living within the urban core by the end of 2021. Meanwhile, more than 80 million square feet of commercial office space is repopulating, and another 10 million square feet is being built or in planning. The expanded residential base and a steadily increasing daytime workforce in downtown Seattle bode well for the economic recovery of retail, restaurants, cultural venues, residential services, and other lifestyle attractions that were shuttered during the darker days of 2020.

From a macro perspective, the Seattle metro area continues to experience the highest aggregate median home price increases in the U.S., posting a 24% year-over-year gain as of August 2021, according to the S&P/Case-Shiller Home Price Index. As attainably priced housing becomes more elusive in outlying areas, in-city condominiums become more attractive.

Seattle entered 2020 as the fastest-growing large city in the U.S., and it’s proving to be the first in and the first out of the COVID-19 pandemic and the related housing disruption in-city. So, with new supply unlikely to keep up with demand, this creates a familiar investment opportunity for in-city condominiums, as it did a decade ago. After the Great Recession, it took five years from the last unit delivery of the past cycle to the first unit delivery of the next market cycle. While the dearth of new condominiums is not likely to be as pronounced this time, the upward pressure on pricing is as predictable, and history is likely to repeat itself.